|

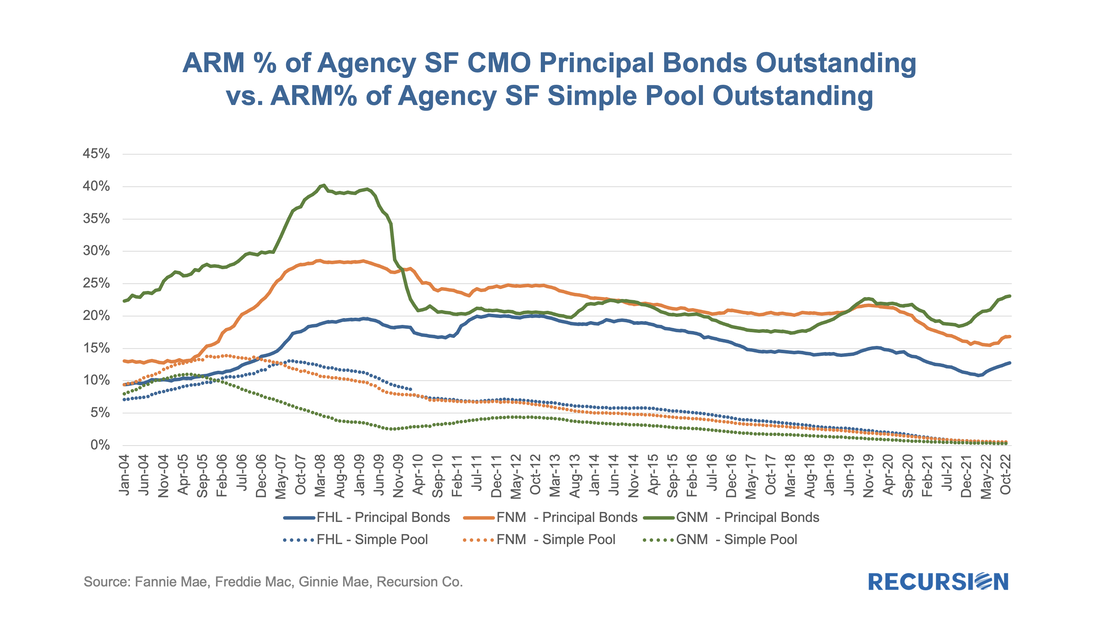

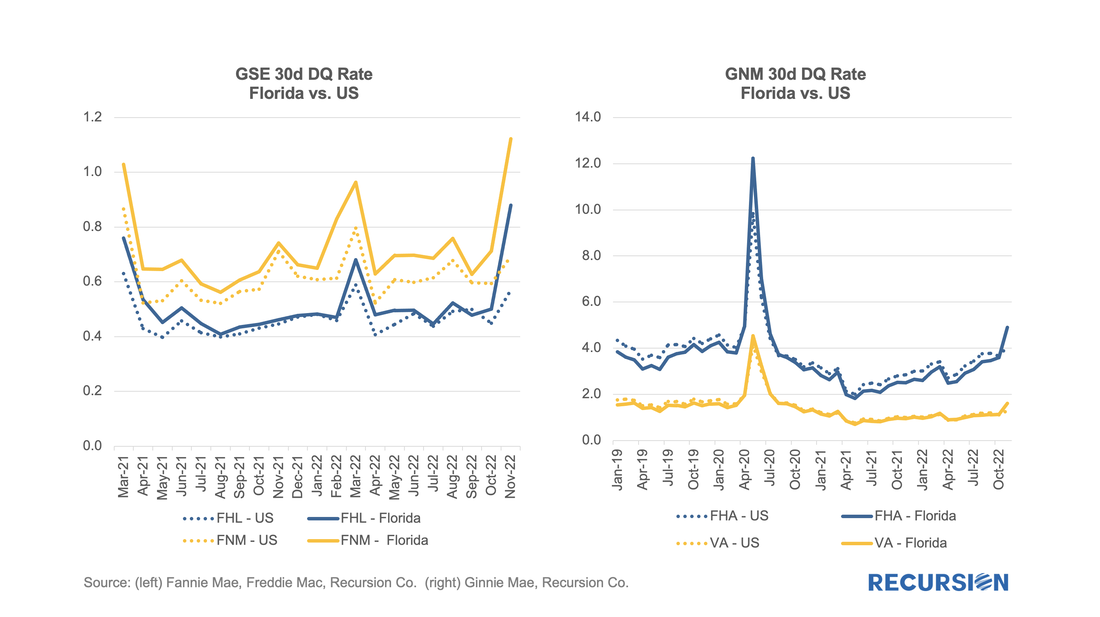

In a previous note, we pointed out that the ARM share of single-family MBS issuance, while on an increasing trajectory, was well below that achieved in prior periods of rising interest rates[1]. There are several possible reasons for this, including bank demand for these types of loans. The new supply (less than 1% of total UPB in recent years) we see in agency pools falls well short of demand for floating rate instruments in the current environment. The solution to this problem comes in the form of financial engineering. Our Recursion CMO Analyzer is a useful tool for examining trends in this market. Pooling financial collateral brings a number of advantages to fixed income markets, notably liquidity enhancement. But there are other benefits to be had as well. First, a CMO can tranche the cash flows from mortgages based on specific factors such as maturity dates and interest rates. This allows investors to optimize their investments with respect to their views on these underlying factors. ARM bonds are popular in these structures relative to simple fixed-rate pools:  As policy interest rates continue to rise and economic activity begins to slow, attention in the mortgage market shifts towards concerns about the potential for borrower distress. We are early in this process as the labor market continues to add jobs, and there continue to be more job openings than people looking for work. Nonetheless, signs of strain begin to be seen, and it's worthwhile to point out early trends and consider implications. Notably, the impact of Hurricane Ian could be seen in the short-term delinquency data:  On November 15, FHA released its annual report to Congress regarding the status of its Mutual Mortgage Insurance (MMI) Fund[1]. The highlight was the increase in the capital reserve ratio by almost 3% last year to 11.11% in 2022. This was the fourth consecutive year of significant growth in this measure of performance. Recursion provided the analytics used to demonstrate successful fulfillment of FHA’s mission, as discussed in Chapter 2 - Access to Credit to Underserved Borrowers. Highlights include:

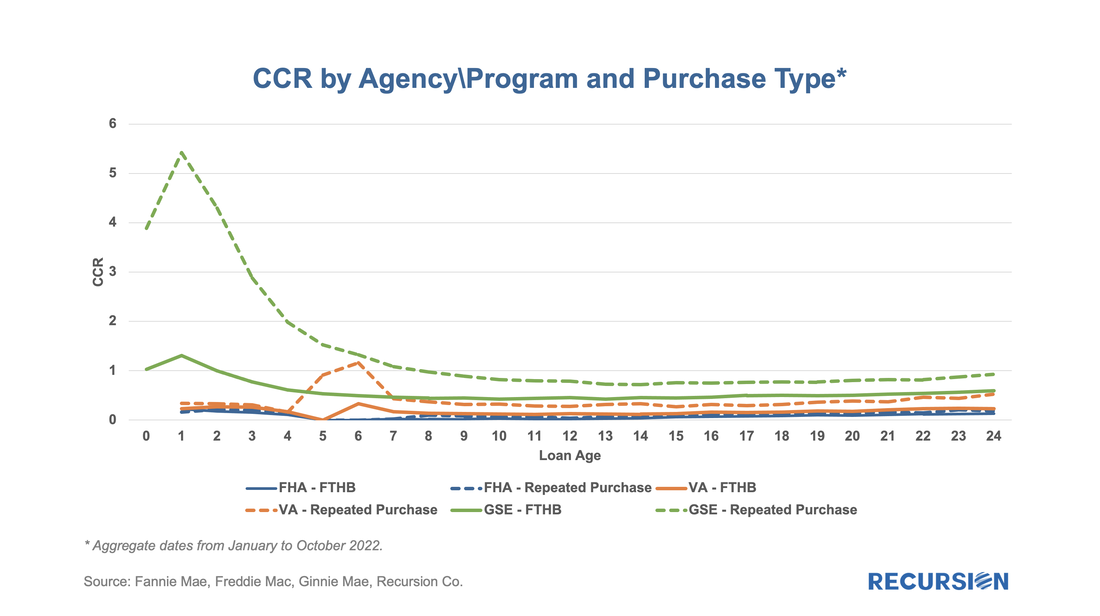

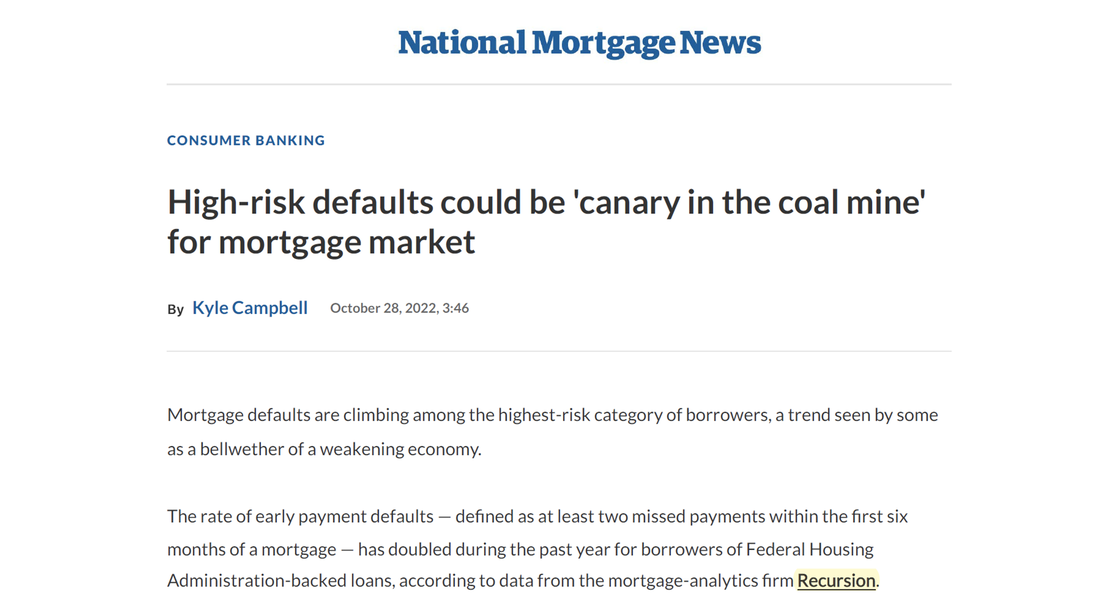

Recursion is proud to be the trusted provider of accurate and timely mortgage data to both public and private sector market participants. https://www.mba.org/news-and-research/research-and-economics/single-family-research/single-family-research-for-mba-members-onlyRecursion is proud to report that it has made an agreement with the Mortgage Bankers Association to make its monthly Top 25 Agency Servicer Report available to MBA members. This report contains data on the size of the serving book, issuance, prepayments, and MSR transfers for the top 25 servicers with 3 years of history., Recursion can provide industrywide data with bank/nonbank shares and reports at individual company level. MBA members can download the report by login to MBA website, and click the link in "Single Family Member Only Research" area: https://www.mba.org/news-and-research/research-and-economics/single-family-research/single-family-research-for-mba-members-only The data are very timely, available on the seventh business day of the month for data through the prior month. Members and nonmembers alike who are interested in the vast amount of underlying information available, including agency, loan purpose, loan size, note rate, underwriting characteristics, geography at the state level, and much more, should reach out to: [email protected] We’ve written before about curtailments, which are particularly interesting during times of rising interest rates when refinancings are at low levels[1]. We believe that investors and modelers would benefit from examining this aspect of borrower behavior. A good way to demonstrate this is to look at the home payment patterns of repeat homebuyers. In the recent environment of skyrocketing home prices, buyers of new homes have been confident about their ability to sell their current residence and have been more likely to purchase their new home before they pay off their old mortgage. If this story is true, we would expect to see significant curtailment activity within a few months of the purchase of a residence on the part of repeat buyers. In our previous note, we introduced the concept of a “Constant Curtailment Rate”, and implemented the calculation in Cohort Analyzer to quantify this effect:  Recursion analysis of trends in short-term delinquencies of Ginnie Mae programs was highlighted in a recent article in National Mortgage News entitled "High-risk defaults could be 'canary in the coal mine' for mortgage market". "The rate of early payment defaults — defined as at least two missed payments within the first six months of a mortgage — has doubled during the past year for borrowers of Federal Housing Administration-backed loans, according to data from the mortgage-analytics firm Recursion." The article goes on to quote our analysis that this trend is notable for lower credit score articles in the FHA program. This has occurred in a period of robust job market, raising the issue that delinquencies may rise further if the recent hike in interest rates by the Federal Reserve results in stalled growth or a recession. Again, more market participants are turning to Recursion to obtain the most up-to-date insights into mortgage market trends.  The article can be found here. (Subscription may be required)

For more information, please reach out to [email protected]. HousingWire cited Recursion data in a recent article discussing MSR risks. “Over the first nine months of this year, banks have far outstripped nonbanks in buying up MSR packages. Banks have been net purchasers of MSRs, to the tune of $107.8 billion — compared with $51.1 billion for all of 2021, according to a report by mortgage-data analytics firm Recursion.” Citing our analysis showing growing short term delinquencies picking up recently, Chief Research Officer Richard Koss is quoted: “It’s a source of concern I don’t think is broadly understood. The main mitigating factor is the still-huge amount of equity most buyers have in their homes.” Recursion is devoted to bringing the most up-to-date data and analysis to support the market’s assessment of key trends and policy issues.  If you would like a copy of the article, please click here

|

Archives

July 2024

Tags

All

|

RSS Feed

RSS Feed

RECURSION |

|

Copyright © 2022 Recursion, Co. All rights reserved.