|

With affordable housing for Low-Moderate Income (LMI) households at the top of the policy agenda, we take a look at loan data for manufactured housing (MH). In a recent report, the CFPB provided a comprehensive survey of this market based on enhancements to the HMDA data first made available in 2018[1]. These include data on Secured property type:

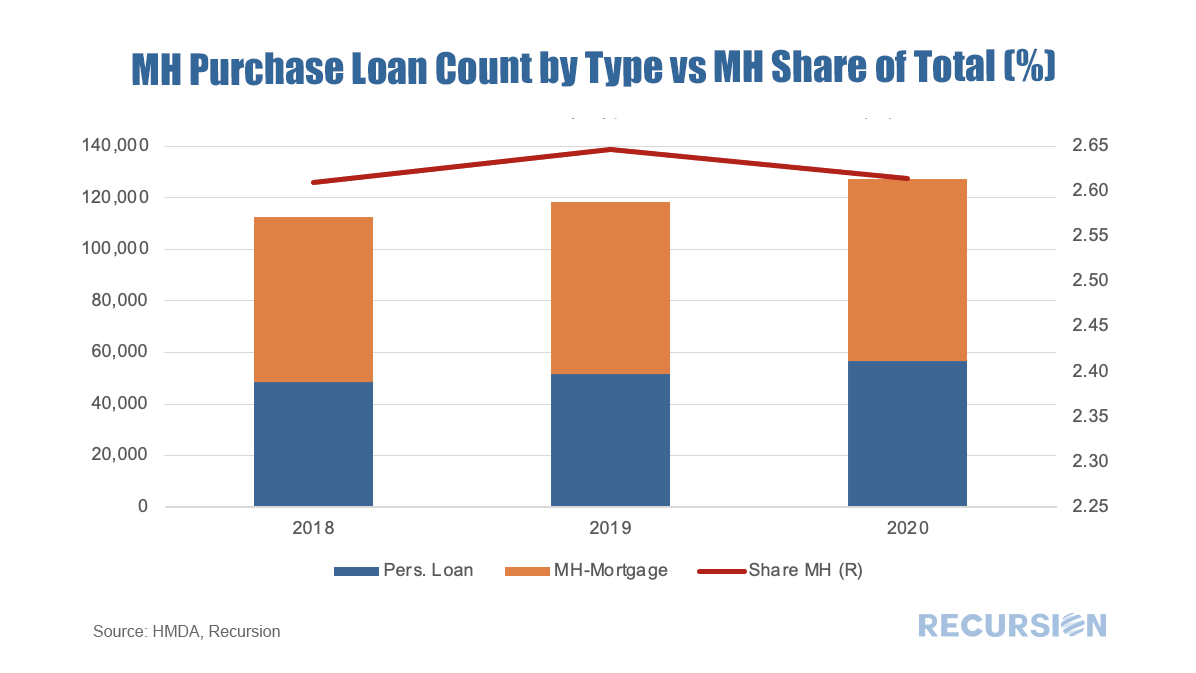

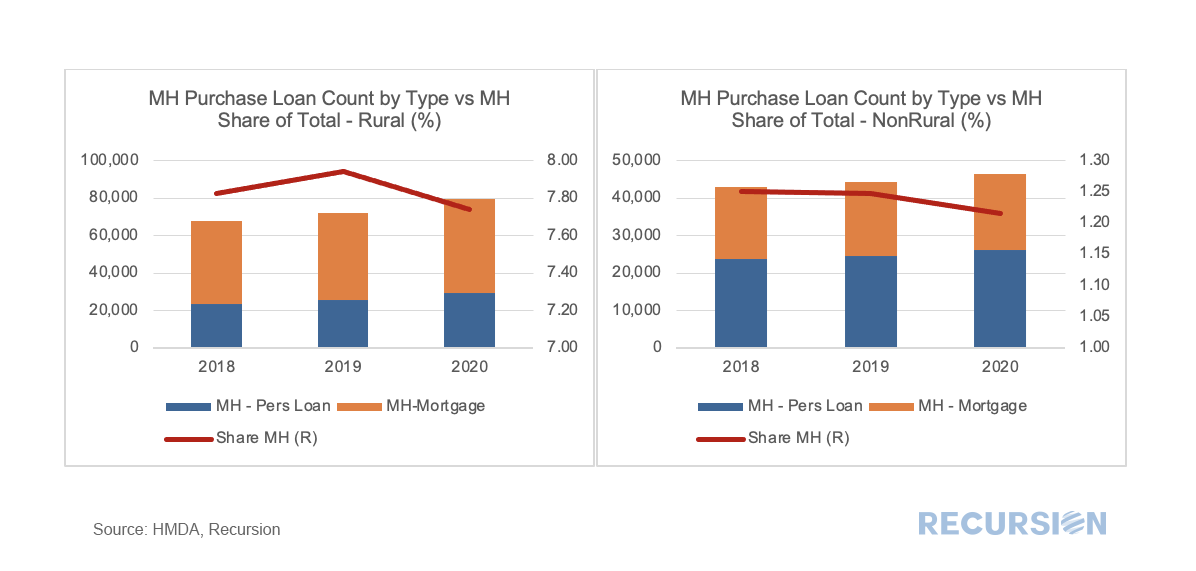

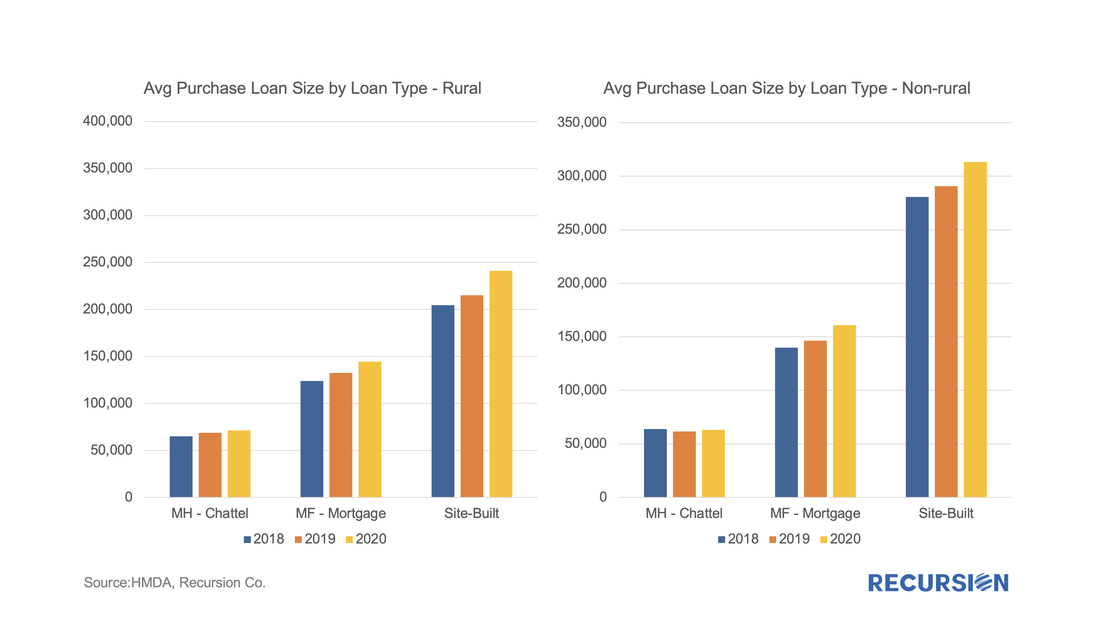

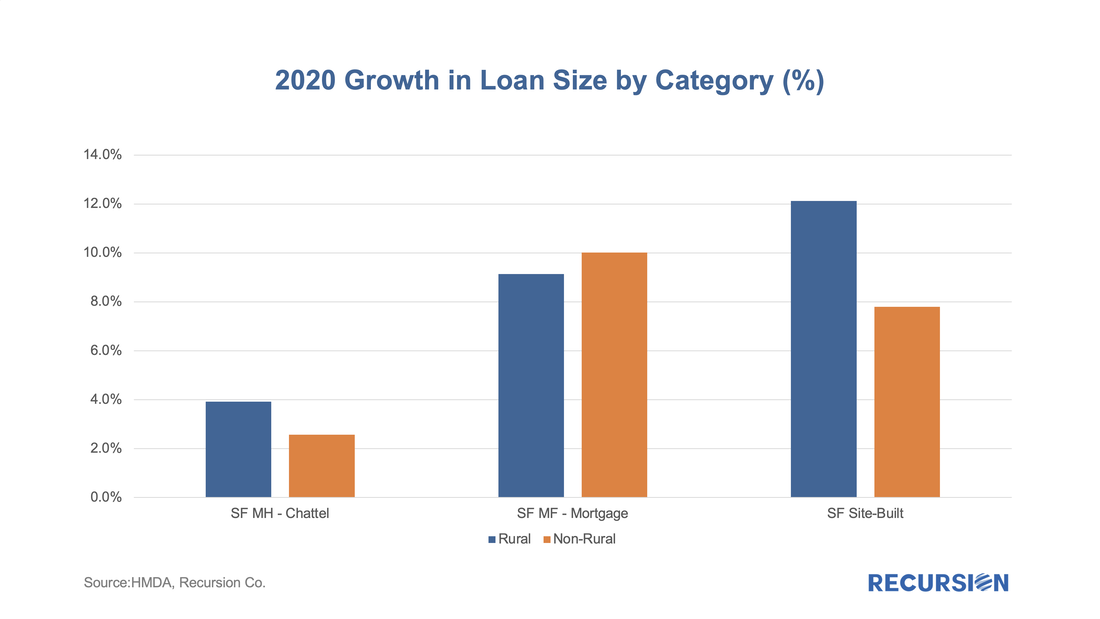

In their survey, the CFPB looked deeply into the data for 2019. In this note, we update some of their work with 2020 HMDA data. This is important because of the onset of Covid-19 that year. The site-built market performed strongly, but this cannot necessarily be presumed to carry over to MH as Covid is a supply shock, impacting labor markets and supply chains. Another innovation in this note is that rather than looking at this market by state the way the CFPB does, as a policy guide we look at it bifurcated between rural and nonrural MSAs. Below finds a chart of the progression of single-family manufactured housing origination volumes for personal loans (securitized by chattel) and mortgages (securitized by real property) from 2018-2020, along with the share of all single-family manufactured housing loans (personal loans plus mortgages) of the total single-family mortgages including those for site-built homes.  Both volumes of personal loans and mortgages for manufactured housing rose in 2020, but the overall share of the MH market posted a very slight dip. The share of the loans for chattel out of all MH loans rose by a modest 1.2% to 44.1% last year. Similar charts can be drawn for rural and nonrural markets, and here there is some distinction[2].  In the rural market in 2020, 7.7% of all single-family underwriting is MH, compared to just 1.2% in non-rural MSAs. Within the MH space, purchase loans with chattel as collateral made up 37% of MH lending last year in rural areas, while in nonrural areas the figure was 56%. Finally, we turn to average loan sizes in rural and nonrural areas.  Unsurprisingly we see that loan sizes are uniformly smaller in rural areas for each category compared to non-rural areas. However, in our prior post [3]on the rural market we noted that loan size changes in 2020 when the pandemic struck were larger in rural areas relative to those in non-rural areas. Breaking this down between site-built and MH, we find that this result does not spill over to chattel loans or MH mortgages.  |

Archives

July 2024

Tags

All

|

RSS Feed

RSS Feed

RECURSION |

|

Copyright © 2022 Recursion, Co. All rights reserved.