|

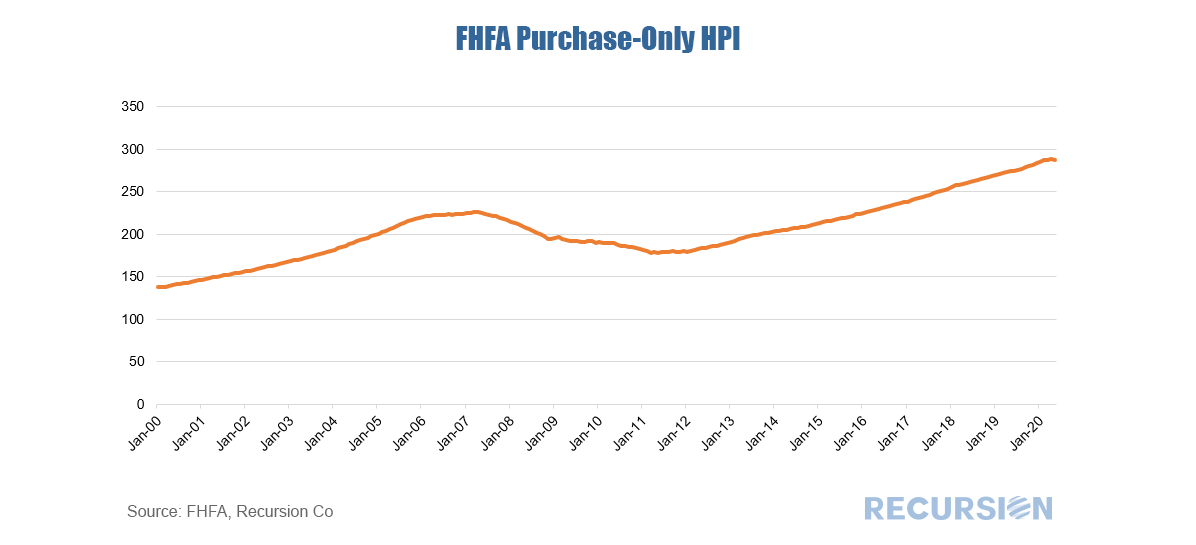

Late last month, FHFA released its purchase-only national house price index for May. This is an index of home prices associated with purchase mortgages that are delivered to the GSEs. The historical pattern is familiar.  In “FHFA’s Capital Rule is a Step Backward”, Jim Parrott, Bob Ryan, and Mark Zandi comment on the FHFA’s recently proposed capital rule for Fannie Mae and Freddie Mac, which requires the two entities to hold capital at least equal to a certain percentage of their total assets [1]. The authors conclude that this proposed framework would lead to higher mortgage rates, lower market share for the GSEs, higher GSE credit risk exposure, and a less stable housing finance system. The authors used Recursion data to demonstrate the impact of mortgage rate changes under the proposed capital framework on mortgage market shares. The paper is accessible through the link below: https://www.economy.com/getlocalq=298f7a13834466aa81c0b495a99f6bbc&app=eccafile With the CARES (Coronavirus Aid Relief and Economic Security) Act offering forbearance to households with mortgages for up to a year, the onus of payments to mortgage investors falls on the mortgage servicers. Much concern has arisen about the ability of these institutions, particularly thinly capitalized nonbank servicers, to meet these obligations[1]. In the case of Ginnie Mae servicers, the PTAP (Pass-Through Assistance Program) was rolled out to provide a line of credit to servicers in Government programs, notably FHA (Federal Housing Administration) and Veterans Administration (VA). In the case of the GSE’s, no such program has been forthcoming and instead, FHFA (Federal Housing Finance Agency) the regulator of the Government Sponsored Enterprises, Fannie Mae and Freddie Mac, announced that servicers of loans insured by these enterprises is only required to pay investors for the first four months if a loan is in forbearance[2].

|

Archives

February 2024

Tags

All

|

RSS Feed

RSS Feed

RECURSION |

|

Copyright © 2022 Recursion, Co. All rights reserved.